SORBUS Spotlight: Think about AI

Few topics in the global economy generate as much excitement as artificial intelligence. It is either the shot up the arm that advanced economies need to return to both pre-2008 growth and to throw off the curse of weak productivity growth. Or, it is the herald of a new age of mass unemployment. Certainly, it has become a near dominant theme for US equity markets.

When trying to assess the hype, there are two important economic factors to keep in mind. The first is that productivity growth has been exceptionally weak for almost two decades now.

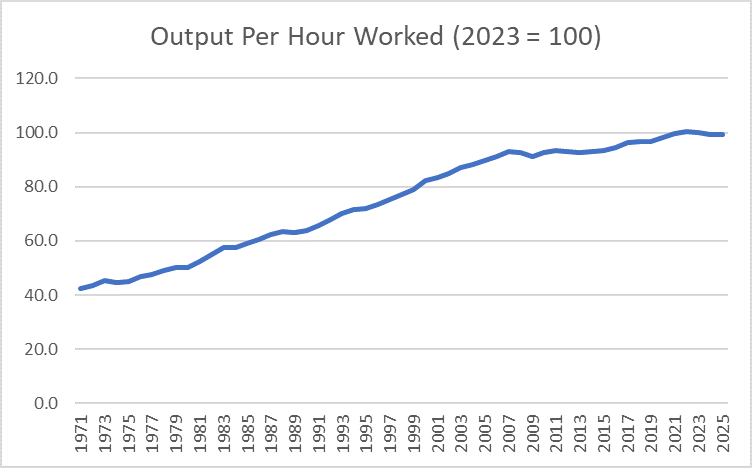

source: SORBUS PARTNERS LLP, ONS (data as at 19/05/2026)

British output per hour worked grew at around 2.0% – 2.5% per annum in the four or so decades until 2008. Since then, the growth rate has slowed to a crawl. It is hard to overstate how much of a problem this is. Unemployment, inflation and wage growth are the kind of things which most people experience in their day-to-day life. Economic growth may be a little more abstract, but fundamentally most people (and most politicians) can get why it matters. Hence, the broad political consensus amongst most major parties across all countries is that faster economic growth would be a good thing.

But without productivity growth, there is no growth in GDP per head. Productivity growth is the key to modern economies, the ability to get more outputs from any given level of inputs. For reasons lost to time, the go to example for economists discussing how production increases is widgets. But given no one really knows what a widget is, it is perhaps easier to stick to cars.

Growing an economy by growing the number of workers makes intuitive sense. If a car factory doubles its workforce, it is completely reasonable to imagine it can also double the number of cars it produces. A car manufacturing executive who wants to double production can, hopefully, think of better ways to do this than by simply hiring twice as many workers. They might add more robots and machinery to their production lines allowing their current workforce to become more efficient in terms of cars produced per hour at work. Or, perhaps, they could invest in upskilling their existing workforce, or even replacing relatively low skilled workers with more skilful hires. Another option would be to change their working methods, perhaps reorganising production lines and the tasks workers carry out. All of these are measures which may increase the number of cars produced without increasing the number of worker hours required. And, of all of them, the most interesting are those gains in productivity that come from things other than simply increasing the amount of machinery used.

In April 2024, in its annual report on the state of the global economy, the International Monetary Fund (IMF) carried out a useful exercise. It decomposed global growth over the last few decades into its raw underlying components – the growth of labour, the growth of capital and the slightly mysterious remainder, total factor productivity (TFP). TFP is a measure of how underlying technology and of how efficiently inputs are used. Using the IMF’s numbers, between 1995 and 2000, annual GDP growth in the advanced economies was 3.28%. By contrast, between 2008 and 2023, annual growth in the advanced economies was just 1.41%. Of that gap of 1.87%, 0.98% (more than half of the total) can be explained by a falling rate of TFP growth.

This starts to get to the root of the problem facing the post-2008 world. There was a material slowdown not just in both the growth of the work force and investment in new capital, but also in something more fundamental; the equally important rate of efficiency gains from new technologies and techniques.

AI might be the thing that turns this around, a new technology which allows TFP growth to accelerate. The IMF reckons that the roll-out of AI could potentially boost productivity growth by an annual 0.8%, which might not sound like much, but would be transformative over a decade or two. An economy that grows by 0.5% a year and one that grows by 1.3% look rather different after ten years – the first has expanded by just over 5%, while the second has expanded by almost 14%. This difference only widens over larger time spans.

AI being able to boost the output of the average worker by 0.8% a year does not seem too large an ask, and indeed the real optimists think something much higher is attainable. But what about the supposed downsides of AI? The fear that AI will throw thousands of workers onto the scrapheap and lead to mass unemployment? Here, it makes sense to be sceptical and to keep in mind that labour market change is normal.

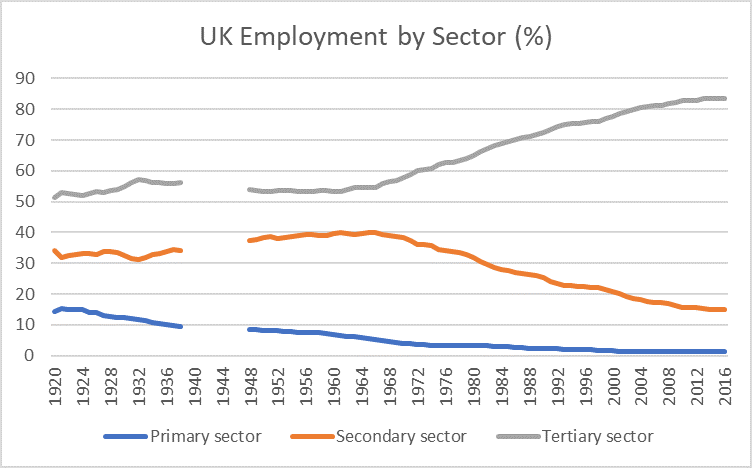

source: SORBUS PARTNERS LLP, ONS (data as at 29/04/2019)

The above chart shows a century or so of change in the composition of the British jobs market. The broad picture is of a decline in primary sector employment (mostly farming and mining), the rise and then dramatic fall in secondary sector employment (mostly manufacturing sector), and the continued growth of the services sector.

To understand this, it is worth keeping a simple economic model in mind. Any new labour-saving technology, be it an industrial robot being installed on a car assembly line, or an LLM model capable of doing the work of a junior lawyer, has, in theory, two impacts. The first is the so-called displacement effect, whereby any half-decent labour-saving technology does what it says on the tin, and allows a given level of output to be produced with a lower volume of labour. Take British farming as one example. Over the last century and half or so, the number of agricultural jobs in the United Kingdom has fallen by around 1.5m yet agricultural output has risen by about 400%.

The second impact is what economists tend to call the compensation effect. If a car factory, for example, brings in a load of new machinery that allows it to reduce its workforce by two thirds and still produce the same number of vehicles then, by definition, the remaining workers will have become three times as productive as they used to be. In the longer run, wages tend to move in line with productivity and those much more productive workers should be able to command higher pay. As their compensation increases, they will go and spend that cash on goods and services, creating demand for new jobs.

In the long run of technological history, the compensation effect outweighs the displacement effect. Yes, a new technology might replace some jobs, but eventually the higher wages associated with higher productivity will create new ones. Mankind has, so far at least, failed to invent anything which has increased unemployment in the long run. This time may of course, to use the most dangerous words in economics, ‘be different’. But betting against 12,000 or so years of economic history is a very brave call. If a trend has existed since the agricultural revolution, it may well have longer to run.

New breakthroughs have tended to cause such worries to be loudly aired. For example, the BBC produced a documentary in 1978 on a new threat called the microchip. The programme warned it would be ‘the reason why our children will grow up without jobs to go to’. Even before the current AI hype train really kicked off, there was plenty of concern. The notion that the robots – or the large language models – are coming for our jobs has been a perennial feature of the last decade. One report from the World Economic Forum in 2016, much debated at their Davos gathering that year, warned that technology would destroy five million jobs by 2020 across the fifteen richest economies. The fact that, on the eve of the pandemic, employment numbers were higher in those fifteen countries than in 2016 did not merit much introspection.

Fears that AI will lead to mass unemployment are almost certainly wide of the mark. Yes, developments in AI might mean, for example, that there is less demand for junior developers and analysts. However, the invention of the spreadsheet meant less demand for human ‘computers’. We didn’t run out of work; we just became spreadsheet jockeys instead.

The thing to worry about with AI is not that it will throw too many people out of work, but that it will fail to live up to its promise – delivering a sorely needed boost to productivity growth.

|

What we are watching. US Inflation, 10th June: US gas prices flirted with $4.50 a gallon in May and that will be reflected in the CPI inflation figures. A rise is inevitable, but more interesting will be the trend excluding energy prices. A rise in core inflation will close down arguments for rate cuts this year. ECB Rate decision, 11th June: the European Central Bank has long been the most hawkish of the major central banks – at times, over-eager to hike in the face of even mild inflation. If any major central bank is prepared to hike in the face of an energy price spike, it will be the ECB China, 16th June: the 16th June sees the release of two important Chinese data series – retail sales and industrial production. The gap between them is worth watching, the trend in recent months has been weaker retail sales (reflecting weak domestic demand) coupled with strong industrial output (as exports surge). |