Market commentary: 1st April 2026 to 30th June 2026

While the surface of the sea can be battered by violent storms and chaotic waves, just a few meters below, the deep currents continue their steady, unrelenting flow.

The Middle Eastern conflict has captured the media narrative over the last three months, with articles discussing oil price and inflation fears an almost daily occurrence. Yet underneath the inexorable driver of stock markets has continued to be corporate earnings growth and the relentless capital expenditure (CAPEX) on Artificial Intelligence (AI) build out.

The FTSE All World index, a broad index representing the global stock market, is up 11.5% for a sterling investor from the 1st of January to 30th June.

The end of Q1 marked the outbreak of the war in the Middle East, sparking an initial sell off. We spoke in our Q1 commentary about how the outbreak of conflict tends to cause a knee jerk sell off in equity markets followed by a broad recovery and in Q2 this pattern has repeated; client portfolios ended June ahead of where they stood prior to the outbreak of the conflict in the middle east.

The real point of interest for long term investors is the AI narrative. It is undeniable that in the short term the CAPEX spend is real and it is a key driver of economic growth and corporate earnings in the US. The question remains, however, over how moored to reality the expectations around the economic impact of AI are?

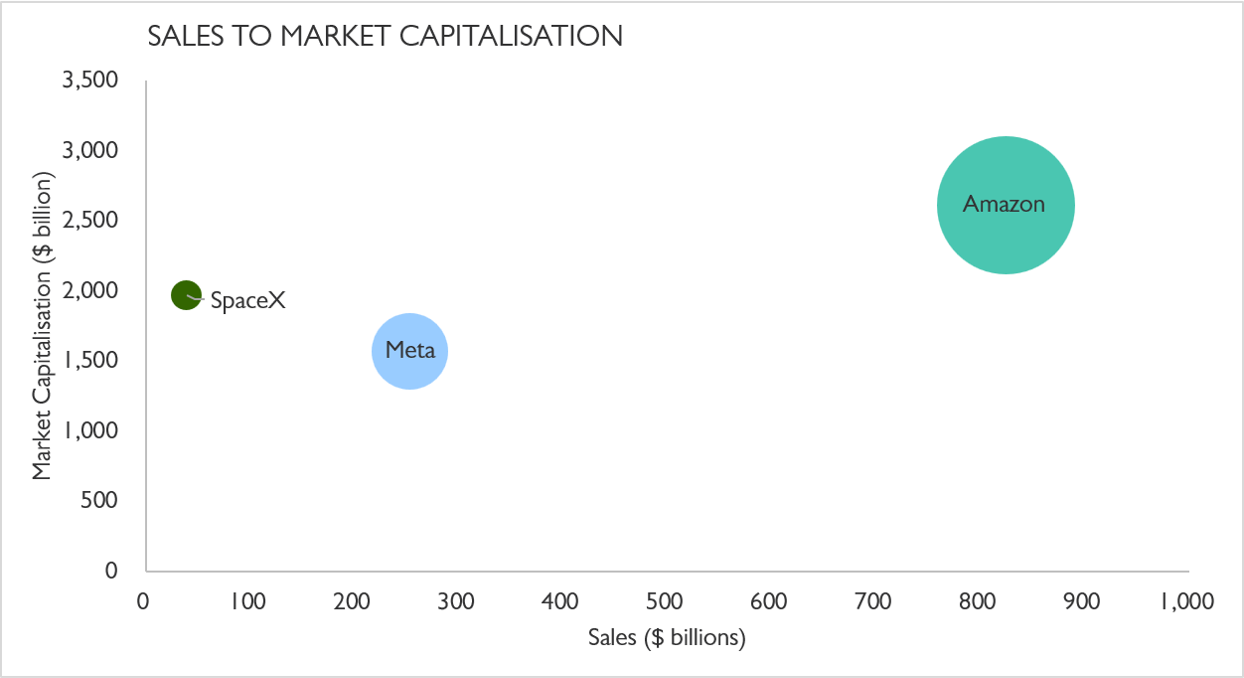

SpaceX provides a case study of this phenomenon. SpaceX represents the largest stock market IPO (the listing of its shares in the public stock market) in history, briefly gaining a market capitalization of $2 trillion. To give this some context we can compare SpaceX to two familiar names in the AI race: Amazon and Meta.

source: SORBUS PARTNERS, Bloomberg (data as at: 16/07/2026)

It is worth reflecting on the prospectus that SpaceX filed for its IPO. Amongst the treasures therein:

- The company claimed a total addressable market of $28.5tn; $26.5tn of which was from AI. US GDP, a measure of annual economic activity, is currently £32.4tn.

- The business plan requires AI revenues to grow from $3bn to $322bn. In four years.

- Morgan Stanley forecasts that Starlink will do £687.7bn of revenue in 2040. Last year this division had revenues of $11.4bn.

- The long term incentive scheme awards the founder, Elon Musk, 1.3bn shares should certain targets be achieved. These include getting the market capitalisation of the company to $7.5tn. They also include the completion of non-earth data centres, which is certainly a first. Also, none of these awards will be paid out unless the company establishes a colony on Mars with at least 1m inhabitants. Obviously.

As the late, great Charlie Munger once commented, he does not want to own shares in Tesla but he does not want to short it either. Elon Musk is a strange human but his ability to attract investors with his ambition and story-telling is phenomenal. We have never considered the valuation of Tesla attractive and the valuation of SpaceX is similarly unattractive.

The chances of this business plan being executed, in these timelines, is so small that one should rationally massively discount the probability of achievement and therefore the value you would attach to the business. We do not believe that any entrepreneur would be persuaded to buy a loss making business with a miniscule chance of achieving its plans at a price that assumes it has already achieved them all. In investing terms it is called “priced for perfection”.

The current situation is the most similar set of circumstances to the dotcom boom since that ended in 2000. There is a difference this time; most of the publicly quoted companies engaged in AI are highly profitable, highly cash generative companies (think Google, Amazon, Meta and Microsoft). However, the AI build out has turned these companies from asset light businesses into asset heavy businesses – data centres are expensive and time consuming to build. The valuation of these companies does not reflect this.

Rising US corporate earnings estimates have been the key support for US equities, overwhelming concerns over the conflict in Iran. However the sustainability of these profits requires the massive investments in data centres, silicon chips and AI software to be value generating in aggregate. This is most unlikely. There will be winners and losers for sure but this CAPEX boom is more akin to a game of musical chairs. The hyperscalers (those companies buying billions of $ worth of Nvidia chips) know and have admitted that buying this much computer capacity at this cost is likely to be value destructive, but they see AI as a “winner takes all” bet. So far their shareholders are allowing them to place these unlikely bets.

The dotcom boom and earlier investment booms all led to over investment. Some estimates of the dotcom period suggest that 85%-95% of all the fibre optic cables laid went unlit (unused). Whilst this overinvestment eventually paved the way for the development of the streaming services we enjoy today, it was only after many of the telecoms companies laying the fibre went bust.

It is also revealing to consider the funding of these data centres. In broad terms, the start of this investment frenzy was funded by cash that these cash rich companies had on their balance sheet. After this diminished they started raising corporate debt. When investors began to get cold feet about the scale of the debt issuance (Alphabet, Amazon, Meta, Microsoft and Oracle have issued $125bn of debt so far this year) then prices of this debt fell. That led to the hyperscales forming joint ventures with the big private credit firms so that it appears that the funding and risk is borne by the credit house (reader: it is not). These large credit firms are now seeing massive redemptions from investors. Finally the companies are now reverting to issuing shares because, at these valuations, it is sensible to do so as well as the last option (other than changing strategy). Alphabet raised $80bn in June and the SpaceX IPO raised $75bn. It has been estimated that SpaceX will require an average of $84bn in external capital next year for each of the following eight years. The forthcoming IPO’s of Anthropic and OpenAI will raise more as will the rumoured equity issuance from Meta.

As a side note in February Alphabet issued some debt that had a 100 year maturity. Taking a century-long risk on funding a massively capital intensive project in its infancy is another reason why we find insufficient value in corporate debt and prefer sovereign debt.

There is clearly a speculative frenzy in AI. Should there be any significant set back for the sector no one can possibly say they did not see that coming. There are more red flags than a Soviet military parade.

For clarity we do not own any shares in SpaceX for our clients, nor will we be participating in the IPOs of the other AI companies. It is our expectation that investors in these businesses will, in the coming years, lose a very significant portion of their investment. The return from any investment, however attractive, depends on the price you pay.

The major change we made in client portfolios over the last quarter was a reflection of these valuation concerns. In May we took the decision to reduce the overall equity exposure in client portfolios by 10%. We reinvested the proceeds into a short term UK gilt, yielding close to 4%, for the time being.

We expect this defensive positioning to persist over the next three months and most likely for the rest of 2026.