SORBUS Spotlight: The second China Shock

The discussion between the world’s leading finance ministers and central bank heads at the International Monetary Fund’s annual set of Spring Meetings in early April was, unsurprisingly enough, dominated by events in the Middle East and fears over higher energy prices. But if the war in the Gulf had not occurred, it is fair to guess that the topic causing the most consternation would have been what some are dubbing the second China shock.

Twenty or so years ago, in the period immediately ahead of the global financial crisis, one topic which would regularly be debated at IMF get-togethers was the issue of ‘global imbalances’. Or, translated out of economies, it was a worry that countries such as the USA and the UK seemed to be running ever larger trade deficits, whilst countries such as China ran-up ever bigger surpluses.

As any good economist will be happy to explain, there is nothing especially virtuous about a country exporting more than it imports and nothing necessarily sinful about a country importing more than exports. The simple logic of “trade surplus = good, trade deficit = bad”, which occasionally makes its way into the popular debate, is rarely that useful. On the other hand, most economists would also worry that a large and persistent trade deficit (or surplus) points to something being out of balance in an economy.

Fears about lasting imbalances, in particular about Chinese trade, are nowadays back in vogue.

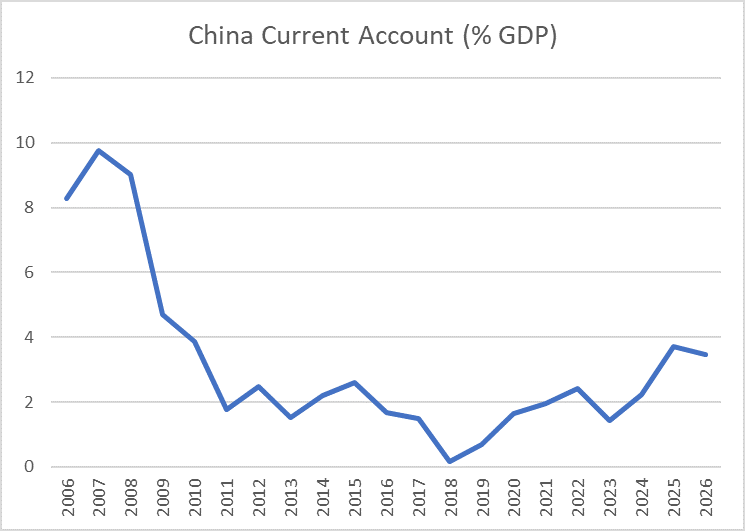

source: SORBUS PARTNERS LLP, IMF (data as at: 20/04/2026)

The chart above shows China’s current account balance as a percentage of GDP. The current account is a wider measure than the simple trade balance. Whereas the trade balance simply measures the value of exports of goods and services minus those of imports of goods and services, the current account aims to capture other financial flows, such as income flows between residents in one country and those abroad. For example, the British current account is made not up not just of Britain’s long standing trade deficit, but also of; the net remittance of profits from foreign owned businesses in the UK back to their home nations, the flow of government payments abroad, any remittances sent by foreign workers employed in the UK back to their families at home. In other words, the current account surplus (or deficit) is a broad measure of payments with other countries. A surplus country is taking in more money from its involvement with the global economy than it sends out, and a debtor nation is doing the opposite.

China’s surplus, as is clear in the above chart, reached very large levels in the early to mid 2000s. Any surplus or deficit larger than around 3% of GDP, especially one lasting several years, is the kind of thing which tends to have close watchers of the data raising an eyebrow or two.

More recently though, it has begun to rise again. By 2019, before the pandemic, China’s current account surplus had fallen to under 1% of GDP, but it is now comfortably back over 3%. Of course, that looks materially lower than in, say, 2006. But China’s economy is much larger than it was twenty years ago.

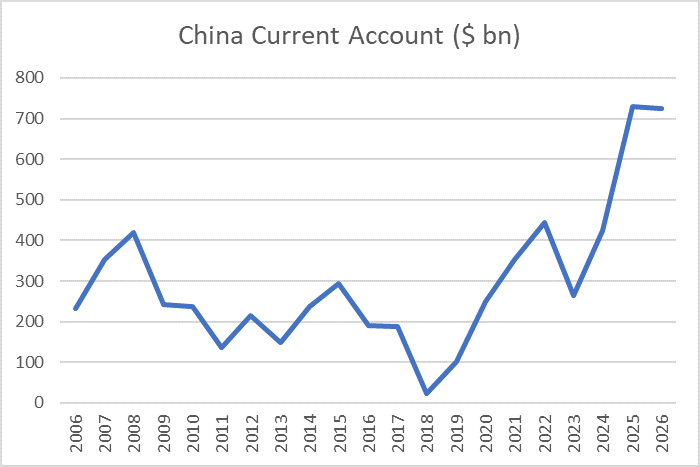

source: SORBUS PARTNERS LLP, IMF (data as at: 20/04/2026)

Putting the numbers into dollar terms makes that clear and explains why global policymakers are becoming increasingly concerned.

Before the pandemic, China was running a surplus with all other global nations of around $100bn. Nowadays, it is over $700bn. That is, even in global macroeconomic terms, a large number. And one that looks set to keep on growing.

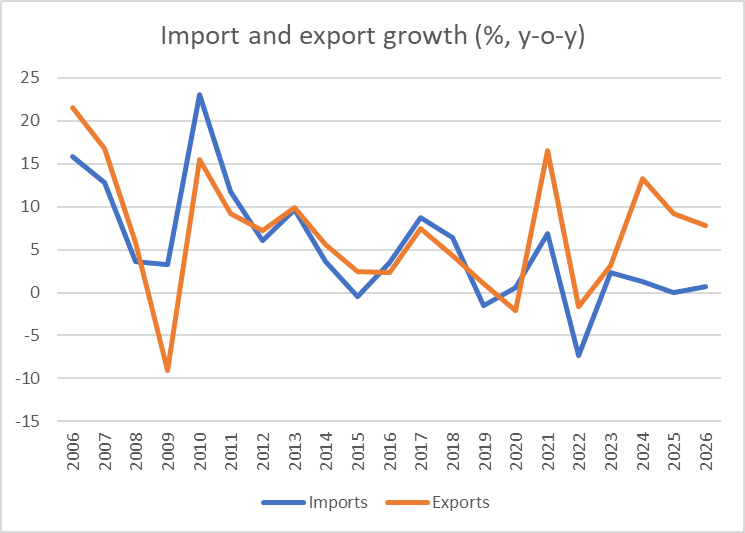

Analysts note that China’s trade data shows an unusual pattern.

source: SORBUS PARTNERS LLP, IMF (data as at: 20/04/2026)

To be clear, the above chart uses IMF data, as China’s own data likely understates the issue. This chart shows the annual change in the value of imports of goods and services vs. exports of goods and services. Most of the time, such measures move together. Higher levels of imports are usually matched by higher levels of exports and vice versa. In China though, since the pandemic, these have decoupled.

Between the end of 2023 and the end of this year, the IMF expects Chinese export volumes to rise by around 30%, while imports barely budge at all. The second largest economy in the globe growing its exports by a third in just three years, without a compensating rise in imports, is a very big deal.

What on earth is going on?

The answer starts with the Made in China programme unveiled as part of the communist party’s medium term economic plans in the later 2010s. That was a conscious effort to lower the foreign made component of Chinese exported goods, and to step up the global value chain. When the pandemic hit, China doubled down on this programme, investing – by some accounts – more than a trillion dollars in building up manufacturing capacity.

The best evidence for the programme meeting many of its goals is to be found by looking closely at the cars one sees in a car park or on the motorway.

The single best-selling new car model in the United Kingdom in March, according to the Society for Motor Manufacturers and Traders, was the Jaecoo 7, with more than 10,000 registrations. Described as a “Chinese speaking Lexus” by Top Gear magazine (or, uncharitably, as a “Temu Land Rover” by some wags), this large SUV retails for around £30,000.

It was not that long ago that seeing a Chinese made car on the British roads was a very infrequent experience. Now though, Jaecoo is a leading new brand, alongside Build Your Dream (BYD) – the leading Chinese auto firm. BYD opened its first UK dealership in April 2023. In December 2025, it opened its 125th.

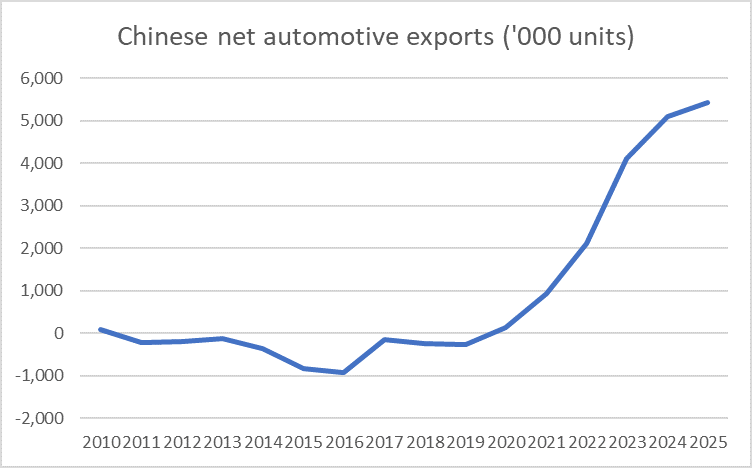

The global picture when it comes to automotive exports is almost staggering.

source: SORBUS PARTNERS LLP, OEC (data as at: 20/04/2026)

As recently as six years ago, China was a net importer of cars. Now, it exports more than five million vehicles annually and has surpassed Germany, Japan, and South Korea to be the world’s largest export of automobiles.

The same can be seen in solar panels or, increasingly, in areas such as machine tools.

The challenge facing global policymakers is stark: China shows no interest in increasing its imports, whilst continuing to grow its exports.

For a country such as Germany, this is a major issue. In the 1990s to 2010s, the terms of the relationship was simple: Germany bought cheap consumer goods from China and exported back high end autos, chemicals, and machine tools. Now, China is making its own machine tools and chemicals and has switched from being a key customer for German carmakers to one of their fiercest rivals.

Even for nations with a lower manufacturing process than the Germans, there is a clear challenge here. While consumers may gain in the short term from cheaper Chinese goods, domestic manufacturing risks being swept away on a tide of cheap imports.

Under Trump, the United States’ response of higher tariffs offers little protection. Even much higher levels of tariffs on China have simply led to Chinese exports being routed via third parties.

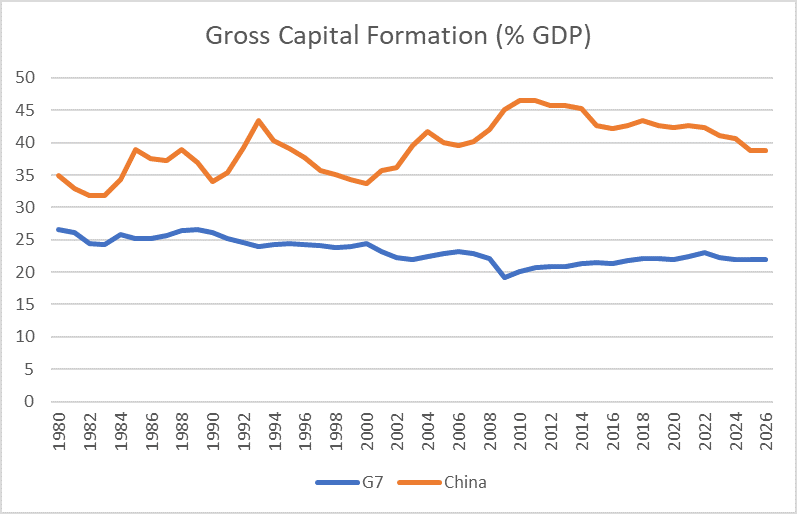

China’s economic model is simply very different from that of the major Western advanced economies. The clearest demonstration comes, in chart form, with a look at capital formation. What percentage of annual economic output is reinvested in capital – whether that be buildings, plants or machinery?

source: SORBUS PARTNERS LLP, IMF (data as at: 20/04/2026)

The G7 nations devote around 20% of their output to investment and consume the rest. China invests around twice as much.

Market mechanisms in the west guard against such high levels of investment – much of which is no doubt wasted or inefficient. State controlled banks provide no such check in China. If the Party decides that, say, car making is a priority area, then cheap loans can be funnelled into building capacity and losses absorbed for as long as they need to be.

One issue, readily identified by the IMF, is that China’s currency is far too cheap. The country has long maintained capital controls which prevent the yuan from rising or falling on an open market. The extent of undervaluation varies by estimate, but is usually within a broad range of around 20 to 30%.

A yuan revalued to be around one quarter higher would make a material difference to Chinese export volumes. If the price of a Jaecoo 7 began at £37,500, rather than £30,000, would it really have shifted 10,000 units in the UK in March?

In a rational world, the US and Europe would be presenting a joint front to China – arguing that unless it revalued its currency and increased imports it would face co-ordinated tariffs and restrictions. But such a united front seems rather far away. US tariff policy swings wildly and without much consistency, the European Union struggles to agree a position acceptable to all of its 27 member states, let alone agree with the United States.

In the absence of an agreed position, a second China shock – much like that of the early to mid 2000s – risks crashing over European and US manufacturing. In the short to medium term, that may help lower inflation. But in the longer run, it would not bode well for any firm in any sector targeted by China’s national plans.

|

What we are watching. The Strait of Hormuz: The best advice is to ignore the political noise and watch shipping volumes. Until volumes materially pick up, a longer lasting energy price squeeze is a risk to global growth. |