IRAN UPDATE

The risks that scare people and the risks that kill people are very different.

The situation in Iran is causing some disruption to financial markets. While this is in its early days and clearly has scope to develop, the lesson of history is that we should not expect any enduring or material impact on financial markets. The Middle East has been unstable for much of the last fifty years and indeed it is hard to find periods of stability in that region in history books.

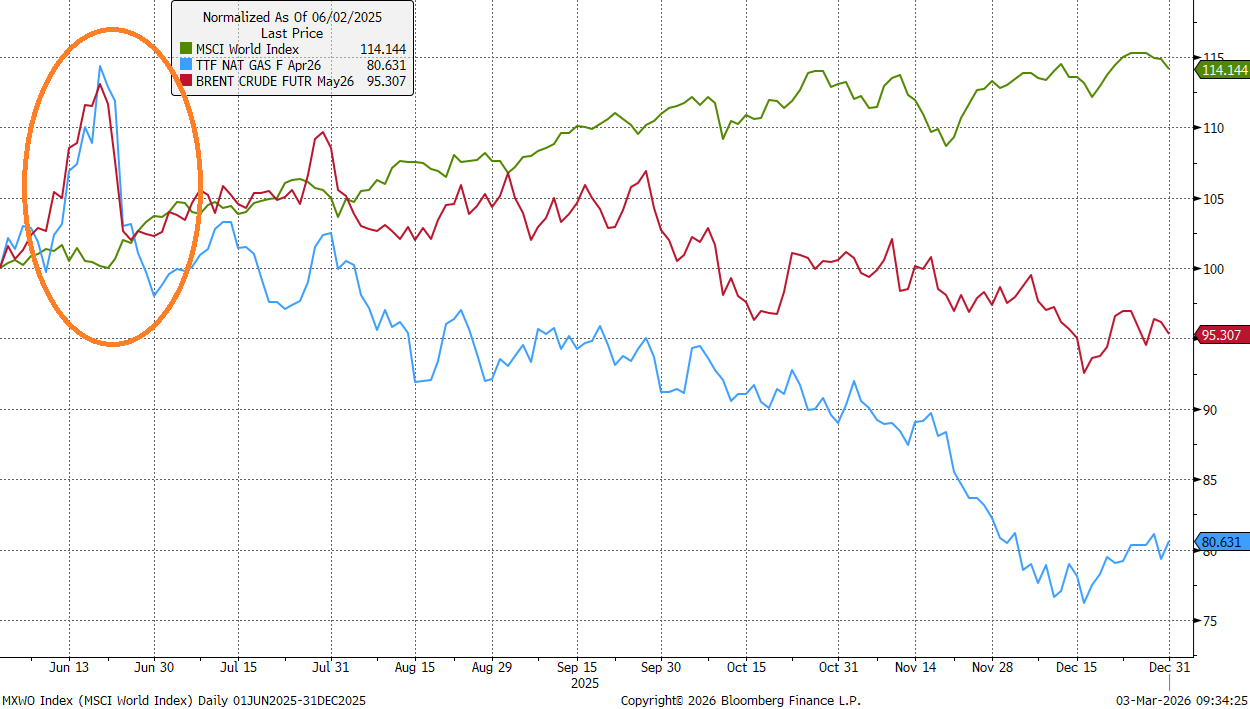

Recent history is supportive of a sanguine approach: in June last year Israel, joined by the US, engaged in a series of military strikes against Iran. The orange circle in the chart below highlights the initial market response to the conflict: equity markets down, oil and gas prices up. Fears around the strait of Hormuz being closed dominated news headlines.

By the end of the month, however, the situation had reversed: all three assets were back to their pre-conflict levels. By the end of last year the Israel and Iran war was no more than a footnote to markets. The story in equity markets was still all about AI, whilst gas and oil prices were both down for the year.

figure 1: Israel-Iran 12 Day War: impact on oil, gas and equity prices (prices rebased to 100)

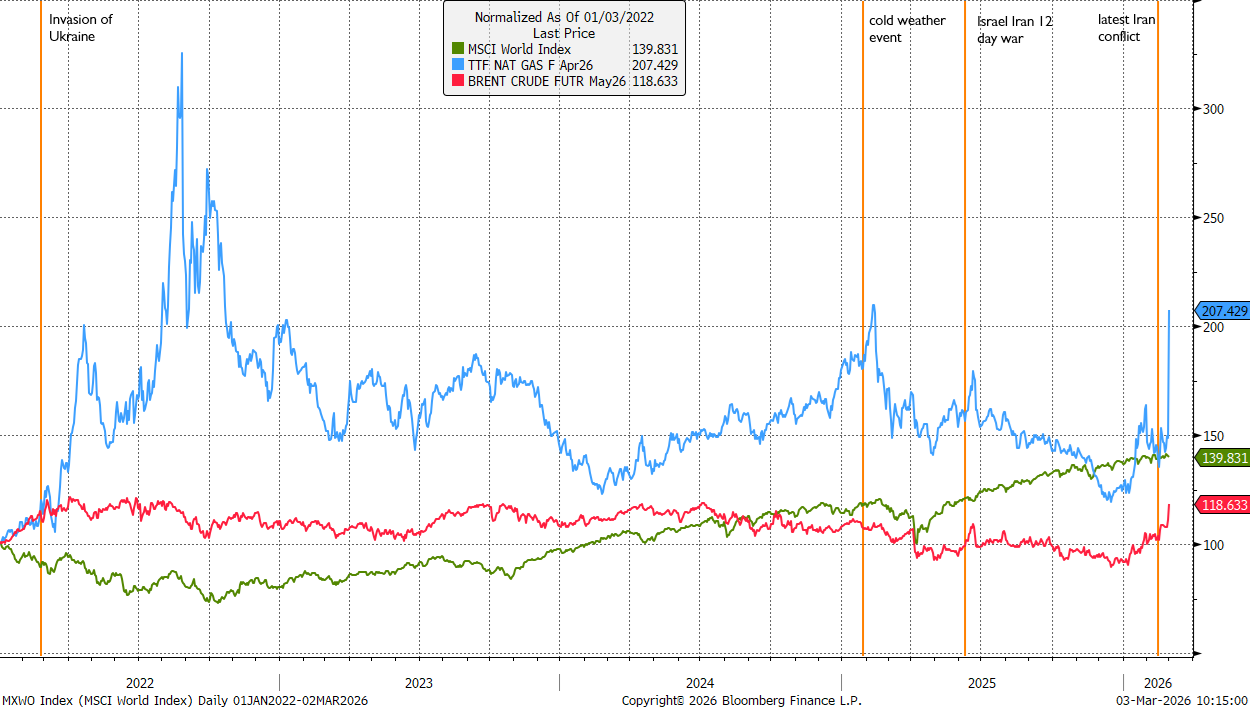

figure 2: Russian invasion of Ukraine: impact on oil, gas and equity prices (prices rebased to 100)

A limiting factor in the argument that “this could be important” is scope. This is not an invasion of Iran. The US infantry has not been mobilised and is not en route. This is a decapitation of the theocracy in the hope that it will lead to regime change. The last intervention of this nature (the arrest of Maduro in Venezuela) also had a limited impact on the global economy. Iran is more enmeshed into the affairs of its neighbours and has spent decades projecting malign power in the region and beyond, so conflict with US aligned neighbours is likely. Iran’s capabilities to project beyond its borders appears limited to supporting terrorism; it does not seem to have the ability to cause any significant military threat while the US maintains this presence.

The flow of oil through the Strait of Hormuz is clearly sensitive to this tension. Iran has leverage to inflict pain on the West via oil price rises and disruption, and will play this weak hand as hard as it can. The US cares much less about this now than it ever has. It is now largely self-reliant on fuel and while price rises rebound globally, absent supply constraints, the US economy will be undented by this.

What this conflict reveals is Trump’s willingness to undertake courses of action that are unpredictable in both methodology and direction. What is predictable is Trump’s wholly personal perspective on politics. He has no real ideology to speak of, he views nations and leaders through the prism of his personal interactions with them. Certainly in 2026 it is not wise to be on Trump’s “naughty list”, much as being on Jeremy Corbyn’s Christmas card list should be a cause of immediate concern (Hamas, Maduro, Iranian regime etc.). However, this is not new. Trump’s behaviours should be reasonably priced by markets because they are understood and markets are, under normal circumstances, exceptionally good at pricing risk.

Fundamentally, what drives asset prices are estimations of how much profit an asset will deliver over time. The conflict in Iran does not have the characteristics of something that will permanently alter the profits of Amazon, Apple, Unilever, Tesco etc. As such, the muted response of markets is appropriate.

Certain asset classes are more exposed; as well as the price of oil and gas rising, history would suggest that we might expect to see some strengthening of the US$, as usually happens in times of conflict. There will likely be continuing strength in gold and other defensive assets. Conflicts deliver uncertainty, distraction and lower economic growth – the extent of which is highly dependent on the context of the specific conflict, so moderately lower prices of assets are justified.

The conflict in Iran, on the current trajectory, is a risk that scares people; market reactions will likely be disproportional to the actual risk.

We are not aggressively positioned at the moment and should further falls in markets persist with the same contextual backdrop (ie: the conflict is not escalating) then we view the disruption as more of an opportunity than a threat; our defensive assets provide the dry powder. For the time being we are comfortable sitting on the sidelines and looking through the current market volatility.