SORBUS Spotlight: Why Japan Matters

Depending on one’s preferred measure, Japan is either the world’s fourth or fifth largest economy. The International Monetary Fund believes that in 2026, India’s GDP will finally surpass Japan in dollar terms, pushing Japan into fifth place. Either way, it remains one of the largest players in the global economy, yet it rarely receives much attention from global economy watchers. When it does appear, it is more often than not as some form of cautionary tale.

Towards the end of 2025, though, Japan did start to capture a bit more of the spotlight from global investors. And not necessarily for all the right reasons.

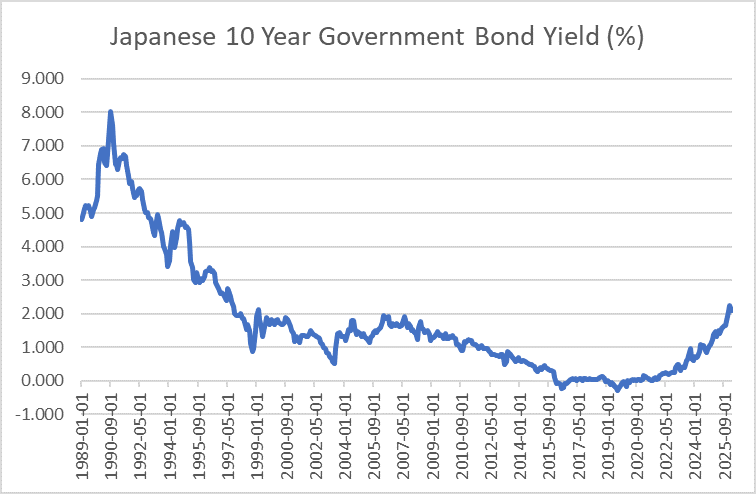

source: SORBUS PARTNERS LLP, FRED (data as at 01/02/2026)

Global bond markets regularly grabbed the headlines in 2025, and often managed to break out of the narrow pages of the financial news. Sell-offs in the market for British government debt, or gilts, caused political wobbles for the government in January 2025 and in the early summer. The single biggest reason for President Trump’s partial reversal of his Liberation Day tariffs looks to have been a serious wobble in the US government bond market last April. Rising French government yields driven by political deadlock and a rough fiscal outlook have regularly spooked investors.

But arguably the most important development in global bond markets in 2025 was to be found in Japan. Beginning late last year, the yield on Japanese government began to rise sharply. Picking up the pace on a drift higher which began after the pandemic.

While the actual level of Japanese 10-year yields, at under 2.5%, remains much lower than the 4-5% range found in the United States or Britain (and even than the 3-4% range found across the Eurozone), two things stand out. Firstly, that this is a major increase from the norm of the 2000s or the 2010s, and secondly, that this is the first sustained move higher in decades.

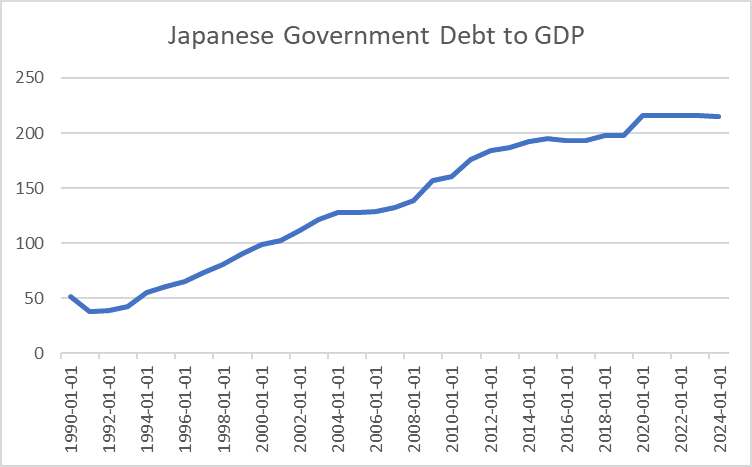

The context which many have reached for is to look at Japanese government debt levels which are, to put it mildly, high.

source: SORBUS PARTNERS LLP, FRED (data as at 01/01/2024)

Government debt levels of more than twice national income, or GDP, may be perfectly manageable when the borrowing cost is near zero – or even at times below zero – but surely they become more of a problem at 2%, 3%, or even higher?

For much of the 2000s and into the 2010s, the market for Japanese Government Bonds (JGBs) was associated with a trade dubbed simply ‘the widow maker’ by global traders. Here was a country which seemed to have effectively no economic growth and ballooning debts and yet whose bonds yielded very little. Surely, went the logic, markets will eventually realise the huge fiscal risks involved and pick to demand a higher premium to hold JGBs. And yet going short Japanese government debt was usually a losing trade, Yields ground remorselessly lower even as debt levels climbed higher, meaning that the price of JGBs continued to rise. Hence the name ‘the widow maker’ – following the usual logic of bond markets was a losing game when it came to Japan.

But how worrying is the rise in JGB yields in reality? Answering that question means grappling with Japan’s real economic problems and also addressing a few misconceptions.

Start with the familiar. Japan enjoyed a post-war boom almost without parallel, before the rise of China.

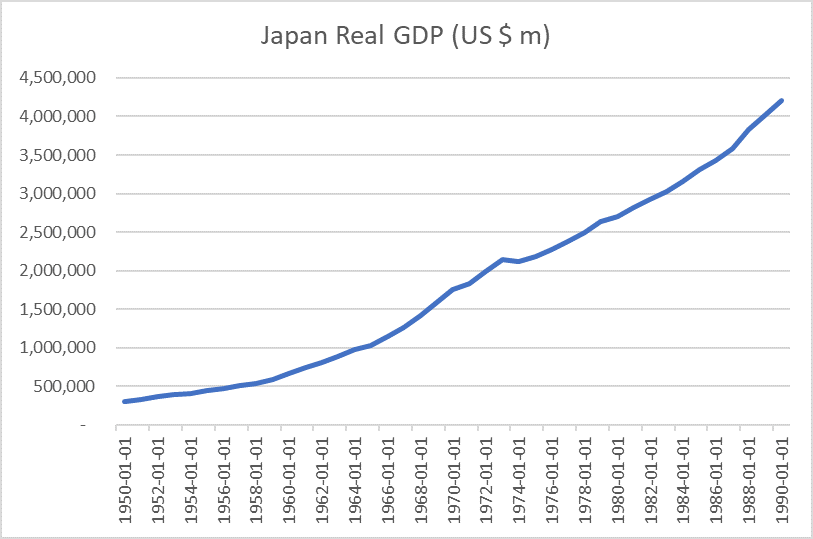

source: SORBUS PARTNERS LLP, FRED (data as at 01/01/2023)

GDP grew to around eight times its 1950 level by 1990. In the 1980s, it expanded in dollar terms by 55% over the course of the decade – with annual growth rates regularly topping 5%, at a time when Europe and North American economies managed more like 2-3%. Japanese carmakers carved out a large global market share and broke into European and American domestic markets in the late 1960s, continuing into the 1970s. Japanese firms dominated the consumer electronics market. Many a book and business school course were organised about learning from Japanese management techniques and, by the late 1980s, the business best seller lists were regularly featuring works predicting that the Japanese economy was on course to overtake that of the United States as the world’s largest by the early 2000s. All of this was accompanied by a major outflow of Japanese capital – opening factories around the world and acquiring a great deal of real estate across the globe. It is notable that the plot of Die Hard takes place in a Japanese owned tower in Los Angeles.

And then came the bust. The growth of the 1970s and 1980s was accompanied by a major domestic real estate bubble and ever more aggressive bank lending to underpin it. Eventually that bubble popped, the stock market crashed, real estate process crashed, and banks were left sitting on large books of poorly performing loans. In some ways, the Japanese economy never really recovered.

Indeed in 2008, as the global financial crisis unfolded, many central bankers looked to learn lessons from Japan in how not to manage a banking and property price crisis. The talk was all of avoiding a ‘Japanese-style lost decade’.

Compounding the financial collapse was a demographic problem. Japan’s demographics appear to be two to three decades ahead of those of the West, with an aging population and a declining birth rate. And, unlike in the West, immigration has remained low and not offered a counterbalance.

Japan is one of the few countries to experience an actual population decline over the last two decades.

It was the Bank of Japan which pioneered quantitative easing, beginning a decade before the Western central banks and creating money at a much more aggressive pace to buy, amongst other things, JGBs. Those low yields which drove the widow maker trade were underpinned by central bank purchases.

Weak growth and poor demographics meant the country spent long periods wallowing in deflation, or a falling price level. And whilst falling prices might sound rather attractive – and certainly preferable to the kind of high inflation experienced since 2020 – sustained price falls are a major problem for an economy. They increase the real value of debt over time, they often lead to firms being forced to cut wages and they encourage both consumers and businesses to delay expenditure and weaken demand further – why buy a new fridge today when it will be cheaper in six months’ time?

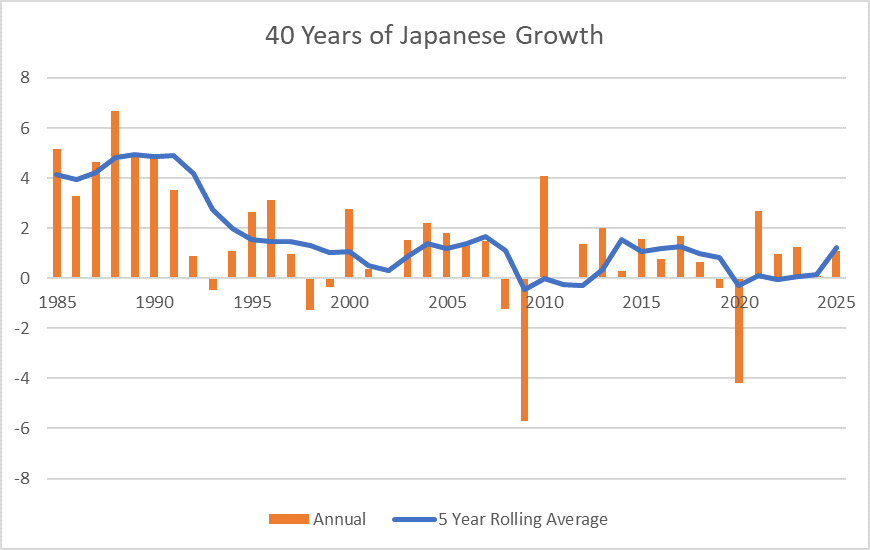

source: SORBUS PARTNERS LLP, IMF World Economic Outlook (data as at 01/10/2025)

The above chart which shows both annual growth and the less volatile five-year growth moving average, gives a sense of the loss of economic momentum.

Since the end of the 1980s, three distinct periods are visible, where growth, over a five-year time frame, began to pick up. The first was in the early to mid-2000s and driven mostly by exposure to rapid Chinese industrialisation. That was snuffed out by the financial crisis of 2008-09. The second was in the early 2010s, as Prime Minister Abe threw the kitchen sink at reviving growth with a package of fiscal loosening, more aggressive monetary stimulus, and a programme of structural reforms. Again, that eventually petered out amid political deadlock. The most recent has come since the pandemic. It remains to be seen though how much of that is simply the impact of a bounce back from a very weak 2020.

Japan’s new Prime Minister, Sanae Takaichi is seeking to revive the Abe-era programme. It is her pledge to cut taxes and increase borrowing to pay for it that has rattled JGB markets over the last few months.

It is easy to see why a pledge to finance tax cuts through borrowing has pushed yields up – a debt to GDP ratio of over 200%, a less supportive central bank in an era of global supply shocks, and a backdrop of three decades plus of weak growth.

But while the most alarmist of observers are warning of a Lizz Truss style market shock in Japan, a few things are worth keeping in mind.

Firstly, for all the focus on lost decades and weak headline growth, it needs to be remembered that Japan’s population growth has often been negative.

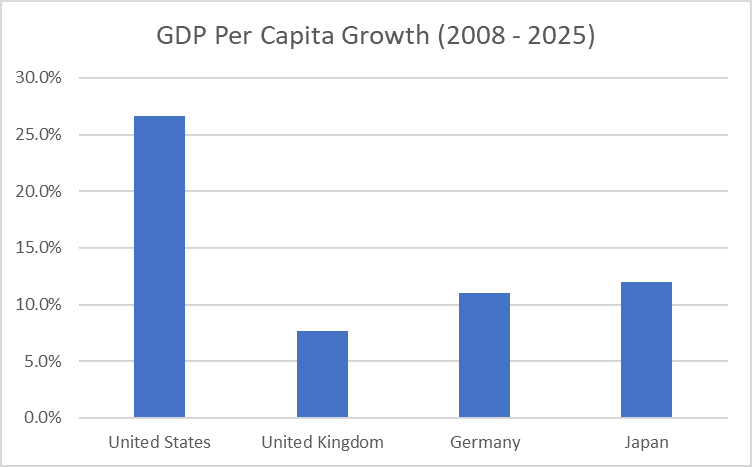

Secondly, the GDP per capita performance since the financial crisis of 2008 is hardly excellent but is also not too shabby.

source: SORBUS PARTNERS LLP, IMF World Economic Outlook (data as at 01/10/2025)

Indeed, on a per capita basis, Japan has outgrown both the UK and Germany over the last couple of decades.

Nor should that 200% government debt to GDP ratio be seen in isolation. Private debt to GDP has fallen considerably since the 1990s, and more importantly, the focus on Japanese government gross debt misses that it also holds many financial assets.

“The analysis produced several novel findings.

- First, as of the second quarter of 2024, Japan’s net public liabilities on the consolidated balance sheet amounted to only 78% of GDP. While gross liabilities stood at 270% of GDP, the government also held substantial assets totalling 192% of GDP.

- Second, a significant portion of these assets were invested in high-return, riskier assets such as domestic equities, foreign equities and foreign bonds. Liabilities primarily consisted of low-return instruments like bank reserves and government bonds. This resulted in a return spread between government assets and liabilities. Despite having a net liability position, the high returns on riskier assets exceeded the government’s funding costs, generating a substantial positive return on Japan’s balance sheet.

The analysis showed Japan’s public sector balance sheet earned an annual return that exceeded its funding costs by exceeding 6% of GDP between 2013 and 2023. The large annual net return explains why Japan’s net liabilities have increased at a much slower rate than its government debt.”

In other words, Japan’s government’s net liabilities would be lower than that of the United States and many European nations if it was to sell the vast quantities of financial assets it held. And, importantly, the value of its assets have long grown faster than the value of its liabilities.

What is more, Japan’s Net International Investment Position (NIIP) – the total value of the country’s holdings overseas versus the claims of foreigners on Japan – is deeply into the black, at more than three trillion dollars.

In other words, the headline Japanese debt figures are nowhere near as worrying as often supposed.

None of which means the new PM’s growth agenda will succeed, but it does mean fears about a financial crisis in Japan are probably overblown.

The rise in Japan yields – if sustained – has the potential to be a big deal for the global economy. Not because it will blow up the Japanese economy but because it means that yield hungry Japanese investors may find they have a domestic alternative to buying American and European bonds. In the long run, the impact of rising JGB yields may well matter more outside Japan than within it.

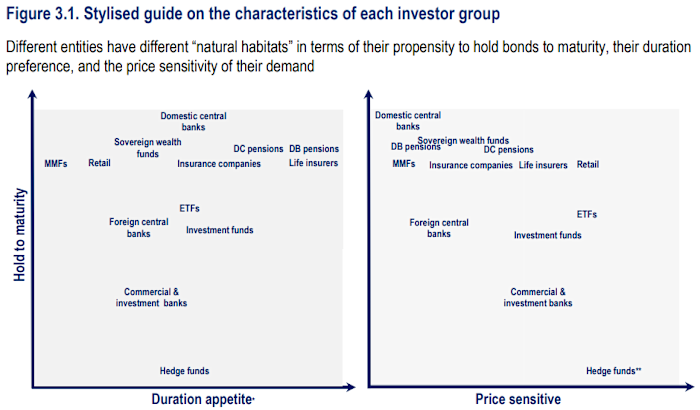

Bonus Chart

An interesting map of how different investors typically behave in the bond market, courtesy of the OECD.

|

What we are watching. The IMF April meetings: the major event on the global economic calendar will be the IMF spring meetings held beginning on the 13th April. The latest World Economic Outlook will provide the first clues to how badly global officialdom frets the war in Iran will impact the global economy and inflation. |