SORBUS Spotlight: What is going on with British inflation?

The public hate inflation. That is one reason why between 2022 and 2024 a record number of incumbent governing parties were defeated when facing re-election. This hatred of price rises is why the government elected in 2024 so regularly mentions what is commonly called ‘the cost of living crisis’ and talks up its own, small, steps to reduce it.

The problem facing both the government, and the Bank of England, is that British inflation remains stubbornly high.

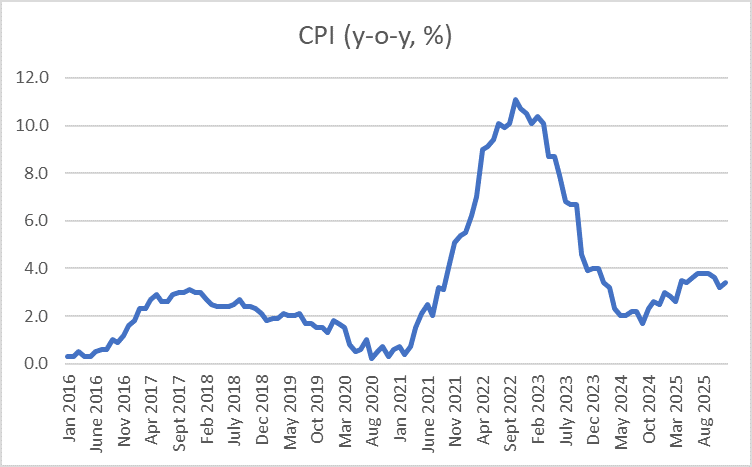

source: SORBUS PARTNERS LLP, Office for National Statistics (data as at 31/12/2025)

The Bank of England hopes to keep consumer price inflation (CPI) around 2.0%. The data at the end of 2025 shows it was running at 3.4%. Worryingly for the government, this is also the first increase in the rate since July.

More worrying still, inflation ended the year around one percentage point higher than it ended 2024. In other words, 2025 was a year in which the ‘cost of living crisis’ intensified.

The tick-up in December was, as many economists were quick to note, mostly due to a series of (hopefully) one-off factors. An increase in tobacco duties and an unexpected spike in airline fares over the Christmas period (a larger spike than normally occurs in the season) both played an outsized role.

The Bank of England will surely argue that there is no case for worrying that this is the start of a new upwards trend. Despite that, there is a strong case to be made that the consensus view of a steady, glide-path back towards 2.0% is overly optimistic.

Indeed, 18 months ago the consensus view on what inflation would be at the end of 2025 was around 2.0%. Instead, inflation rose to 3.8% in Autumn 2025. For all of the government’s talk of helping with the cost of living crisis, it needs to take an outsized portion of the blame.

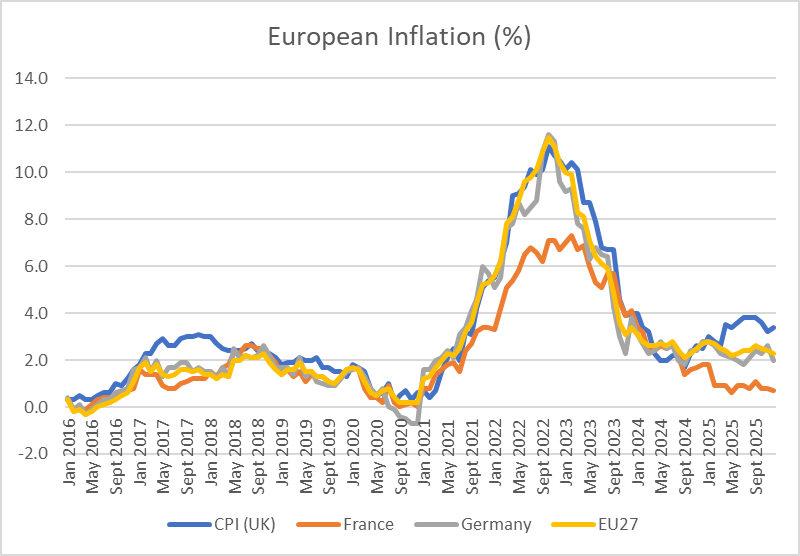

It is worth looking at British inflation rates in conjunction with those of other European economies.

source: SORBUS PARTNERS LLP, Office for National Statistics (data as at 31/12/2025)

The first thing to note is that inflation rates across Europe – mostly – move together. There are of course exceptions. French inflation has tended to be lower than that in either the UK or the rest of the European Union as result of the very different structure of its energy market. With nuclear providing much of its electricity generation capacity, it was much more insulated from the 2021 – 2023 global energy price spike.

Over the last decade there have been two distinct occasions in which British inflation has notably diverged from European rates for a material length of time. The first of these came in mid 2016, until early 2018. For that case, the culprit is easy to identify. Sterling fell around 15 – 20% against the UK’s major trading partners in the immediate aftermath of the Brexit referendum. This put upwards pressure on the price of imports, increasing the general price level, and hence, inflation.

The second divergence is more recent: since the Autumn of 2024, inflation rates in Europe have drifted down, whilst those of the UK accelerated and then remained elevated. The culprit in this case seems to be the then still-new government’s first budget – in particular the large package of tax rises.

Macroeconomics 101 states that, all things being equal (to use an economist’s favourite phrase), a large package of tax rises should reduce inflation, rather than cause it to pick up. Tax rises, after all, reduce the amount of spending power available to both households and firms, and in general, less spending power should mean less spending. Less spending means lower overall economic demand, and a reduction in demand, relative to supply, should mean less pressure for prices to rise and thus lower overall inflation.

The current level of inflation just goes to show that lesson 101 is rarely enough and that all things are rarely actually equal. It is perfectly possible that some tax rises – such as income tax or corporation tax – might have reduced household or firm incomes and hence spending pressure. And the £30bn or so of tax rises passed by the Chancellor’s first budget will no doubt have had that impact. But that was not their only impact. Taken as a whole, the tax rises chosen mostly added directly to the costs of production, causing firms to increase prices to protect often shallow margins. The rise in employer national insurance contributions, the single biggest measure, is a classic example of this. But other tax duties that were hiked – such as VAT on private education or vehicle exercise duty – also added to price pressures.

British inflation has been running around one percentage point higher than European inflation mostly because of the fiscal policies pursued by its government.

That at least provides some hope for relief in the future. The second large package of tax rises, delivered at the budget in Autumn 2025, looks less likely to result in more direct cost pressures. Additionally, once April 2026 rolls around and the year on year base effects of the tax changes that mostly occurred in April 2025 drop out of the comparison, there is some hope that inflation could fall.

But will it fall enough?

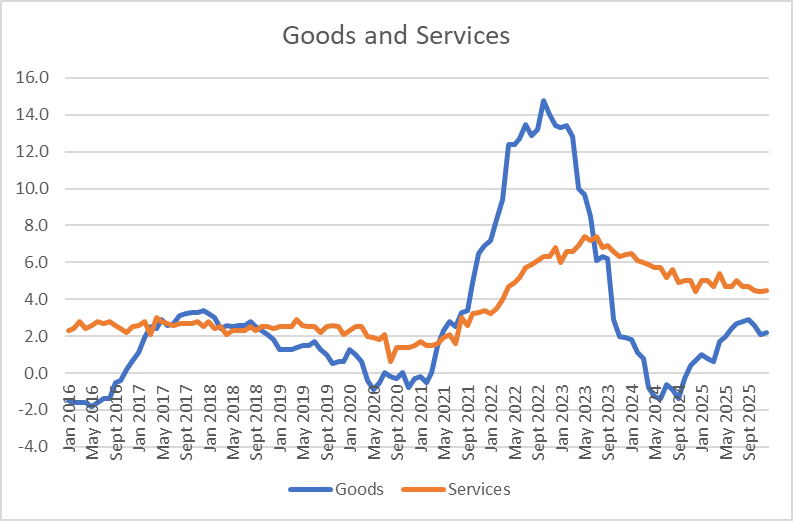

Regular readers of Spotlight will by now know that one useful way to think of British inflation is to simply split it into two components: goods and services.

source: SORBUS PARTNERS LLP, Office for National Statistics (data as at 31/12/2025)

Goods inflation, while it proves the major recent inflationary spike, is in many ways the less interesting part of the story. In general, although not always, goods price inflation is driven by global factors. The state of global demand for energy and food, relative to supply, as well as the health of global supply chains, play an outsized role. The weakness in sterling, which pushed up import prices in late 2016 and 2017, is easily spottable on a goods price inflation chart.

Although goods price inflation has risen over the last 18 months, it remains well within the kind of range long regarded as ‘normal’.

Services price inflation is far more interesting. For a start, it is more domestically driven. Yes, energy prices, which are mostly set globally, play a role here, but the much bigger story is one of wage costs.

Even when goods price inflation leapt upwards in 2016 and 2017, services price inflation remained fairly steady. That was the best reason not to be too concerned about the wider British inflation picture in the immediate aftermath of the 2016 referendum. By contrast, as goods prices soared in 2021-2023 service price inflation also began its own steady rise – to the highest levels since the early 1990s. And even as goods price inflation collapsed, service price inflation only steadily came down. What is more it has remained seemingly stuck in the 4.5-5% range for the past two years, at a rate more than double what was once considered normal.

Unemployment has been rising in recent months and, again if one believes macroeconomics 101, that should reduce wage pressure and hence service price inflation. But, once again, 101 does not seem to be enough. Unemployment may be rising but wage growth remains much higher than before the pandemic, partially as a result of large rises in the minimum wage (and the resulting need to raise other wages to maintain differentials).

The UK then has stumbled beyond macroeconomics 101, with tax rises that add to, rather than dampen inflation, and a slowing jobs market which is not materially lowering wage pressures. That leaves the Bank of England facing something of a quandary in 2026. In normal circumstances, a deteriorating jobs market would be met by a faster series of interest rate cuts. But, as long as service price inflation remains well above 2.0%, it is hard to see further large-scale reductions in rates. There is a reason the market is now only pricing one or two cuts in the coming twelve months.

There will be a lot of noise about British inflation over the coming year. The headline rate could well fall backward to 2.0% in the Spring, if global goods prices remain benign. But, as long as service price inflation remains above 3.0%, there is no case for relaxing. Until service price inflation returns to more normal levels, the chance of a major inflationary upswing cannot be ruled out.

|

What we are watching. Bank of England, 5th Feb – The February meeting of the Monetary Policy Committee also sees the quarterly release of new BOE forecasts. The thing to watch for will be if they nudge up their forecasts for inflation in response to December’s disappointing figures. German industrial production, 6th Feb – Manufacturing matters to Germany but it is still only around 20% of the economy. On the other hand, it now seems clear that consumer confidence will not return without an upswing in manufacturing. The German economy has, after a two year recession, begun growing again. The industrial production figures need to be watched closely. US inflation, Feb 12th – President Trump wants lower interest rates and is not shy of telling this to the Fed. The market seems inclined to ignore this browbeating as long as the US inflation outlook seems reasonable. The problem will come when the White House’s clear desire for lower borrowing costs is more in conflict with the inflation backdrop. |