SORBUS Spotlight: What is going on with the US Economy?

The world’s largest economy is rarely out of the headlines or, indeed, of investors’ minds. Already, 2026 has seen major developments on the data front, the policy front and, this being America, where suing people is the national hobby, on the legal front too.

How is the US economy doing?

A major government shutdown towards the end of 2025 made the US outlook much harder to read. For a start, most of the core macroeconomic data upon which analysts usually rely simply stopped being published. Even once the data taps were turned back on, their output remained a little suspect. The lack of reliable data collection in October and November, for example, casts some doubt on the inflation statistics released in December.

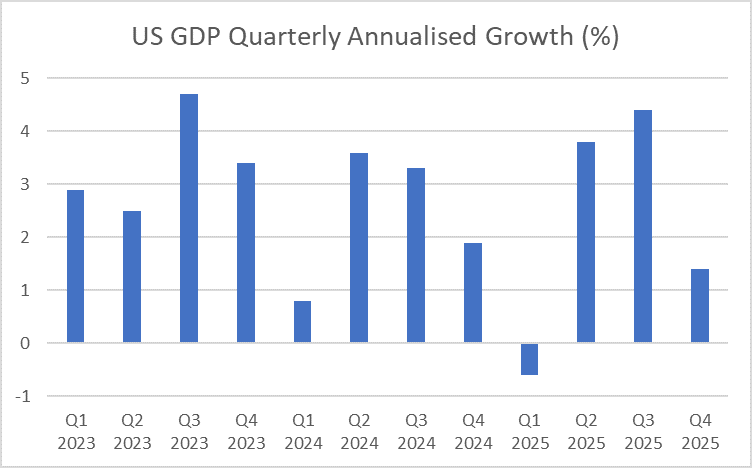

The latest GDP data point to a sharp slowdown in growth towards the end of last year and the numbers came in well below what analysts had pencilled into their forecasts. This, though, is not an especially troubling development. There is little doubt that the Federal government shutdown had a major impact on spending – possibly reducing the annualised growth rate by as much as two full percentage points. And the experience of past shutdowns is that much of that spending will have been delayed rather than cancelled. In effect, some growth will have moved from the tail-end of 2025 into the early part of 2026.

source: SORBUS PARTNERS LLP, US Bureau of Economic Analysis (data as at 20/02/2026)

US economic growth then looks to be continuing at a reasonable pace, and certainly at a faster rate than experienced in Europe.

The jobs market, on the other hand, does not appear so healthy. Hiring remains relatively weak and the pace of job creation looks to have slowed in the second half of 2025, although not by as much as once feared. Inflation remains elevated and above the Federal Reserve’s target. Chairman Powell provided an excellent summary of the current state of the US economy at his January press conference noting that: “the economy is growing at a solid pace, the unemployment rate has been broadly stable and inflation remains somewhat elevated”. That, as he argued, presents the Fed with something of a quandary given its dual mandate to keep price rises and unemployment low, “the upside risk to inflation and the downside risks to employment have diminished but they still exist, so there’s still some tension between the mandates”.

The tariff decision.

Complicating the picture further is the recent Supreme Court ruling on tariffs.

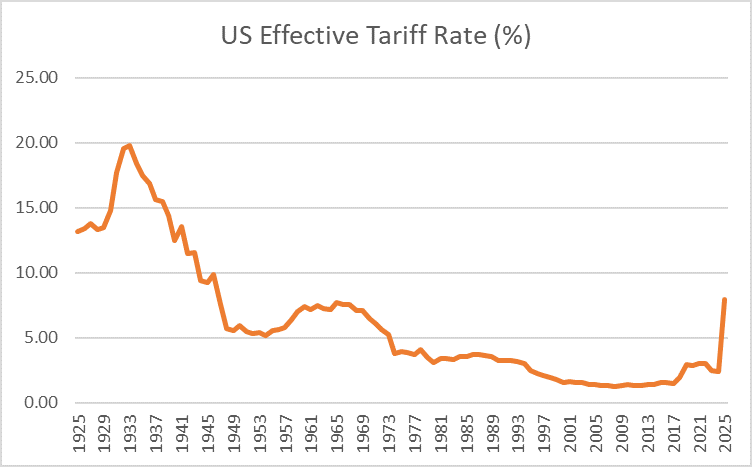

Ten months ago, Donald Trump launched what he dubbed his ‘reciprocal tariffs’ at an event in the White House Rose Garden. The tariffs were, in the main, much higher than what the investor, or just about anyone else, had expected and prompted a sell-off in financial markets. Faced with a falling dollar, rising yields on US government debt and a tanking stock market, the administration paused the tariffs for 90 days, struck a series of detail-light ‘trade agreements’ with other countries and eventually put in place a tariff-package that, while not quite as severe as that initially threatened, still represented the highest level of US protectionism in decades.

source: SORBUS PARTNERS LLP, The Budget Lab at Yale (data as at 20/02/2026)

On Friday 20th February, the Supreme Court ruled that the entire charade was illegal. The 1977 International Emergency Economic Powers Act (IEEPA), which was used to bring in both the reciprocal tariffs of Liberation Day and some earlier hikes in tariff rates on China, Mexico and Canada, does not – in the view of the court – grant powers to the executive. While some of the administration’s tariffs – such as those on steel, copper, aluminium and autos and auto parts – still stood, the vast majority were struck down.

The President’s immediate response, at an angry White House press conference, was typically contradictory. After branding the decision “a disgrace” and calling the justices who backed it “fools”, the President essentially claimed that it made no real difference to his governing agenda as he had alternative tools available. On the 20th February he imposed a 10% global tariff on imports using the authority of the 1974 Trade Act and, the following day, increased that to 15%. Under the 1974 Act, these new duties can remain in place for 150 days. Over the coming months, the administration aims to put in place a new tariff regime, although mostly via more cumbersome processes which typically require investigations before being enacted.

The most immediate economic impact of the ruling, and the administration’s cobbled-together response, is a large injection of uncertainty back into the global macroeconomy. The post-pause US tariff regime may have been high, but it was also relatively stable. Both US importers of goods, and foreign exporters, can no longer be sure exactly what rates they will face when the 150 days of Trade Act tariffs come to an end. That matters. Empirical research has found that elevated uncertainty tends to be associated with weaker corporate investment and lower hiring.

The domestic impacts on America’s own economy are even harder to unravel. For a start, exactly what happens to the $140bn or so collected over the last year under the now-struck down tariffs? The most likely outcome is a large pay-day for trade lawyers as companies sue the government seeking refunds. The pattern of refunds will no doubt provoke plenty of ill-feeling. In many cases, an importer facing a new tariff will have passed on the cost to its own customers, but any repayments will flow to the importer, rather than to the customers who faced higher prices. Investors in US bonds may become a little twitchy if it looks like tariff revenues are going to be materially lower than anticipated, especially as those tariff revenues were one justification given for Trump’s tax cuts.

The largest impact of the supreme court ruling, though, is likely to come in the realm of geopolitics rather than economics. It will take the Trump administration time to rebuild their tariff framework, more legal hoops will have to be jumped through and some not-too-rigorous ‘investigations’ will have to be carried out. But a tariff regime similar, if not identical, to that which existed on the morning of February 20th will no doubt be put back in place eventually. What the White House has really lost, now that the IEEPA tariffs have been ruled against, is flexibility and the ability to move quickly on tariffs.

In the short run, tariff related uncertainty is back. But in the medium to longer term, the inability of the President to change tariff rates should deliver a bit more certainty.

A new Fed Chair?

Arguably in the longer run, the appointment of a new head of the Federal Reserve will be more consequential for the US economy than the ruling on tariffs.

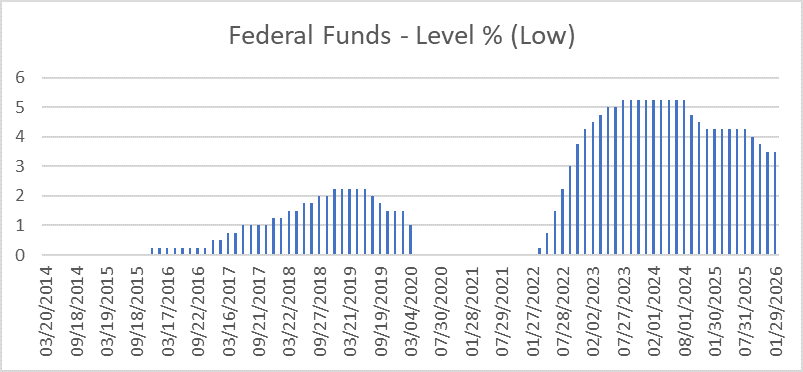

source: SORBUS PARTNERS LLP, Federal Reserve Bank of New York (data as at 20/02/2026)

While the Fed cut rates in 2025, it clearly did not move as quickly as the President would have liked.

The President has made no secret of his belief that interest rates should be materially lower than they currently are and appears to have no time for the usual niceties of avoiding making his preferences clear. In his first term as president he regularly berated the then Fed boss Janet Yellen. However, over the past year his attacks have moved beyond the verbal and rhetorical. His administration has attempted to remove Governor Lisa Cook from the rate-setting Open Markets Committee on spurious charges of mortgage misconduct, he appointed one of his own advisors to the board, and his Justice Department have subpoenaed the current head, Jerome Powell, alleging the mismanagement of a building refurbishment project. For months markets have feared that he would attempt to replace Powell, whose term is due to end, with a stooge prepared to ignore the outlook for inflation and simply cut interest rates to ease Federal borrowing costs and buoy up the economy before November’s Midterm elections. The independence of the Fed itself has been seen as under attack. The real worry, for bond and currency markets, is that a Federal Reserve more concerned with keeping the President happy than with the pace of price rises would result in inflation spiking higher. The end result would be lower bond prices and a weaker currency.

Hence the immediate relief visible in the currency markets, at the announcement that Trump would nominate Kevin Warsh, an ex banker, former Fed policymaker, and market savvy advisor to the President. While Warsh might be close to President Trump, he is also seen as traditionally holding more hawkish views on inflation. When he served as a Fed governor between 2006 and 2011 he often argued for tighter monetary policy and, in the years since, he has argued that the expansion of the Fed’s balance sheet and the policy of quantitative easing (electronically creating new money to buy government bonds) went too far. Over the past twelve months he has towed the President’s line, publicly agreeing with him that interest rates should be lower. This, he has argued, is justified by faster US productivity growth driven, in part, by the development of artificial intelligence.

Investors currently expect some further modest rate cuts from the Fed and, in the near term at least, it is not hard to see Fed-White House relations being on a better footing than in 2025, while financial markets calm down about the risks to Fed independence.

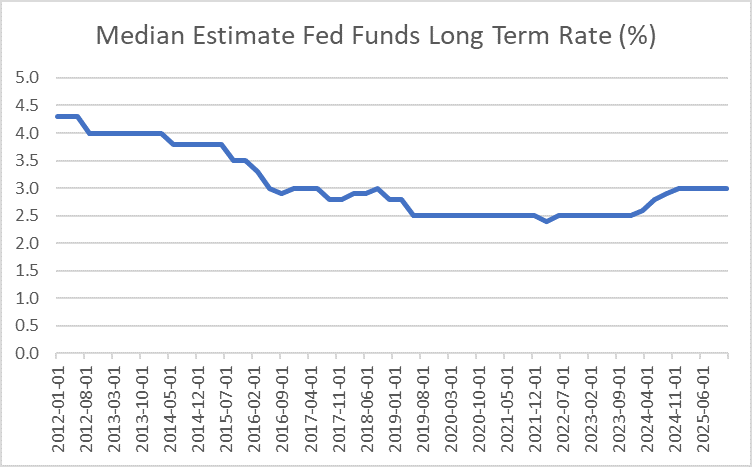

source: SORBUS PARTNERS LLP, FRED (data as at 20/02/2026)

Several times a year, as Spotlight has previously highlighted, Fed policymakers set out their view of the likely long term level of US interest rates. This is probably the best estimate of what they believe ‘neutral’ rates (the level at which interest rates are not causing the economy to either accelerate or decelerate) are. As can be seen, the view of what represented neutral fell in the 2010s and rose sharply after 2022.

At present US monetary policymakers believe it to be around 3%. There is room for further cuts in rates to get back to neutral, but not a huge amount of wiggle room. Chairman Warsh should be able to please the President for a while, but perhaps not for too long.

Summing it up.

At present then, the US is growing at a reasonable clip, but risks are building on the horizon – the jobs market slowdown is a concern, as is the still relatively high level of inflation. An injection of tariff-related uncertainty is unlikely to help in the short term. The reality, though, is neither the booming economy proclaimed by the White House nor the crisis often predicted by President Trump’s opponents. In a word, the US economy is doing just about ‘fine’.

|

What we are watching. US Productivity, 5th March – Kevin Warsh has staked his ability to keep lowering interest rates on the idea that the US is enjoying a 1990s style productivity boom, which would mean even a robust jobs market would not generate as much inflationary pressure. So, US productivity figures have taken on a new level of importance. They will be more closely followed by Fed watchers. Chinese inflation, 9th March – Chinese inflation fell to just 0.2% (year on year) in January, down from 0.8% in December 2025. That is a worryingly low level. Policymakers are fretting about a return to deflation which could depress output and hit hiring. The timing of Lunar New Year almost certainly distorted the figures and the number for February (released in March) should give a steer on how much of the fall reflected the timing of holidays and how much of it was real. Japanese Leading Economic Index, 9th March – Japan’s new Prime Minister, who has pledged to cut taxes and increase government borrowing to give the economy a boost, now has an electoral mandate. The leading economic index, based on surveys of firms, will give an early clue to how her agenda is being received domestically. |